6 Things to Do Before You Buy a Used Car

The car-buying process starts well before you ever start talking to a seller, whether you want to shop at a dealership or find a private seller. To have a good used car buying experience, take a few early steps to find information on your own, and put yourself in a better position when it comes time to make a deal.

1. Set a budget

The first place to start is setting a budget for yourself. Understand how much money you’re willing to spend in total on your car and how much monthly financing will likely cost you. This will help you when you communicate with a seller and as you browse options and makes it easier to narrow down a few options ahead of time.

When you set your budget, you might realize that the right car for you is a little too expensive—and that’s okay. Once you have this information, you can start saving or make another plan to make that car a reality in the future.

2. Pick a car

You want to make sure you find the right used car for your needs. Is there anything about your current vehicle that you wish you could change? Maybe a hatchback will give you better options for a road trip, or your growing family needs a bit more space in the back seat. Gas mileage and repair costs are other important factors to consider as you start your search for the right make and model.

3. Find sellers

The internet is your friend when you start your search for a used car. Local dealerships and private parties post available cars online, so search around to get an idea of where to start your buying process. Looking up your options online first will also give you an idea of whether the car you want and your budget are realistic.

4. Do your research

You’ll also want to make sure you understand what a fair price for the used car in question is. Kelley Blue Book is an excellent tool to figure out how much a used car should cost. Keep this number in mind before you start looking at cars to make sure you’re not being taken advantage of by a seller.

A great thing about buying a used vehicle is that other people have been driving the make and model for some time. This means you have access to more information than you would about a new vehicle. Check out a site like Edmunds to get a sense of how reliable different vehicles are. Some used cars are notorious for their bad reputations, so you can put some on a “never buy” list.

5. Get preapproved for a car loan

Once you know the car for you is out there, it’s a good idea to get preapproved for a loan before you start any negotiations. This is great to have in hand before heading to a dealership because you can avoid negotiating financing on the spot, and you can rest assured that you can cover the cost of owning the vehicle in question with your loan at a rate you’re comfortable with.

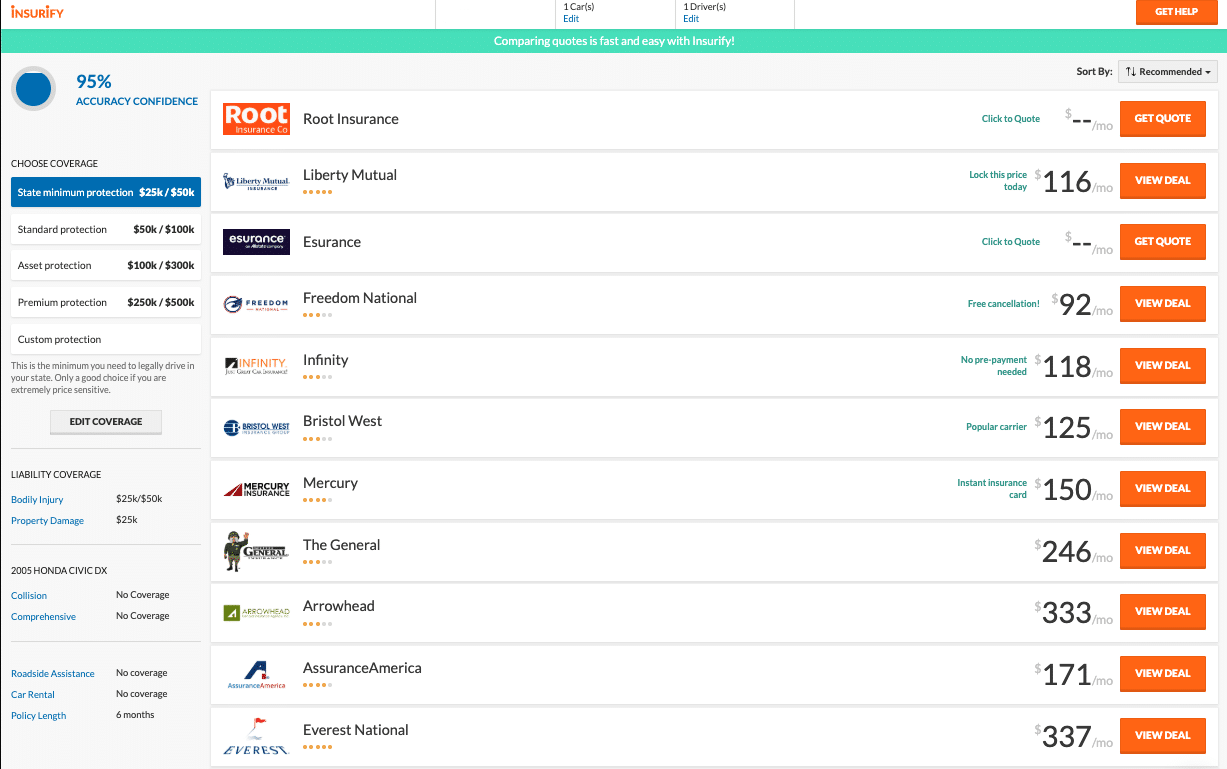

6. Purchase car insurance

Most car loans require you to have a car insurance policy in place before you get preapproved. Even if you already have an active policy, buying a new car is a good time to make sure you’re getting the best rate and policy for your needs. Insurify can help you compare quotes to make sure you get the best rate on your car insurance policy.